A Bill to Increase Foreign Infrastructure Investment (Global Infrastructure Partnership Program) NSDA Congress 2026

A Bill to Increase Foreign Infrastructure Investment (Global Infrastructure Partnership Program)

Orientation. The chamber will want to debate “should the United States counter China’s Belt and Road Initiative?” — and on that question the advocates win in a walk, because countering Chinese influence is bipartisan applause. But that is not what this bill decides. It asks something narrower: should Congress create a new program — the Global Infrastructure Partnership Program — to do a job the United States is already doing through agencies that exist right now? The bill routes its money through the U.S. International Development Finance Corporation, which Congress reauthorized in December 2025 and supercharged from a $60 billion cap to $205 billion through 2031, and it duplicates the G7 Partnership for Global Infrastructure and Investment and the Blue Dot Network the U.S. already leads. The round turns not on whether to compete with China, but on whether this bill adds anything that isn’t already in the field — and whether its one new feature, a loyalty condition, helps or backfires. Control that framing and you control the room.

Part I — The Policy Pro/Con Brief

Why this debate is live right now

Great-power competition over infrastructure financing is one of the defining contests of the decade, and it is moving fast. China’s Belt and Road Initiative now spans more than 150 countries with over $1 trillion in cumulative investment and construction contracts, and 2025 was a record year for new BRI engagement, so the perception of a financing gap the U.S. must fill is politically potent.

The U.S. response is already substantial and recent, which is exactly what makes a new program contestable. The DFC was reauthorized in December 2025 with a tripled cap and broader country eligibility; the G7’s PGII set a $600 billion mobilization goal by 2027 as the declared counter to BRI; and the Blue Dot Network certifies transparent, debt-sustainable infrastructure as an alternative to BRI’s terms.

And the premise underneath the bill — that BRI works by trapping nations in debt — is itself contested. Chatham House’s study of the Sri Lanka Hambantota case found the “debt-trap diplomacy” narrative is largely a myth: the port was Sri Lanka’s idea, the debt distress came mostly from Western capital markets, and there was no asset seizure. That a bill premised on countering debt traps may rest on a flawed premise is what makes this a real debate rather than a reflexive China vote.

The Case FOR the Bill (Pros)

The advocates’ best ground is that the strategic stakes are real, the demand abroad is real, and the United States has a proven vehicle to meet it.

The strategic stakes are genuine. BRI’s $1 trillion-plus reach across 150 countries gives Beijing economic leverage that translates into diplomatic and security influence. A credible American alternative is a defensible national-interest investment, not charity.

There is real demand for a better offer. Many developing nations want infrastructure and would prefer transparent, debt-sustainable financing to opaque terms. A program built on transparent bidding and debt-sustainability standards meets a need that exists.

The vehicle already works. Routing funds through the DFC means leaning on a bipartisan, recently reauthorized institution with loan, guarantee, and equity tools — realistic implementation, not a new bureaucracy built from scratch.

Transparency conditions are a real differentiator. Conditioning support on open bidding and debt sustainability is the soft-power selling point: it lets the U.S. compete on quality and governance where BRI is weakest, rather than trying to match China dollar for dollar.

Private capital multiplies limited federal dollars. Using loans, guarantees, and equity to mobilize private investment — the PGII model — stretches a modest federal commitment into a much larger financing footprint.

Annual reporting builds accountability. The required joint State–Treasury report to Congress creates a feedback loop that lets lawmakers measure whether the program actually reduces reliance on BRI, a discipline many foreign-aid efforts lack.

The Case AGAINST the Bill (Cons)

The opponents’ best ground is not “don’t compete with China” — it is that the bill recreates machinery the United States already has, funds none of it, and bolts on a loyalty condition that backfires.

It is redundant — the currency check is the whole case. The bill’s own administering vehicle, the DFC, was reauthorized and expanded to a $205 billion cap in December 2025, and the U.S. already runs PGII and the Blue Dot Network for exactly this purpose. The bill names a program that substantially already exists.

It authorizes without appropriating. The bill promises “low-interest loans” but specifies no dollar amount and provides no appropriation — it routes through the DFC’s existing authorities and adds no new money, so it is a press release with a program name, not a funded commitment.

The DFC is the wrong tool for “low-interest loans.” The DFC is a development-finance institution that invests for returns and mobilizes private capital, not a concessional lender that hands out below-market loans. The bill asks an agency built on market-oriented returns to do something outside its model.

The loyalty condition backfires. Section 2(A) gives priority to nations that “commit to limiting future participation” in Chinese-financed projects — turning a development offer into a geopolitical loyalty test. Most BRI partners are non-aligned states that refuse binary choices; demanding exclusivity repels exactly the countries the program is trying to win.

The U.S. cannot win a spending race, so scale-matching is the wrong frame. Even the expanded $205 billion DFC cap is dwarfed by BRI’s $1 trillion-plus and record 2025 activity — and this bill adds nothing to that cap. A bill that implicitly accepts a dollar-for-dollar contest sets the U.S. up to lose on China’s terms.

The debt-trap premise is contested. The bill is framed around countering BRI debt traps, but Chatham House found the flagship Hambantota “debt trap” story is largely a myth — so the bill’s animating rationale rests partly on a narrative the evidence doesn’t support.

The agency structure is muddled. Section 3 puts both State and Treasury “in charge” while Section 3(B) routes funding through the DFC — three institutions, no named lead, and a built-in coordination problem before a single project is financed.

How to Weigh It

The strongest pro is that the strategic competition is real and there is genuine demand abroad for transparent, debt-sustainable financing — so a credible U.S. alternative serves the national interest. The strongest con is that the United States is already doing this through the DFC, PGII, and the Blue Dot Network, that the bill funds nothing new, and that its one novel feature — a loyalty condition — is the part most likely to drive partners back toward Beijing.

The crux is whether this bill adds capability or merely renames existing capability. If the room believes the U.S. lacks a counter-BRI vehicle, the bill looks like a serious answer and the debate is about scale and conditions. If the room knows the DFC was just reauthorized to $205 billion and that PGII and Blue Dot already exist, the bill looks redundant and unfunded, and the loyalty condition looks actively counterproductive. Advocates must argue the bill fills a real gap and that conditionality buys leverage. Opponents must show the gap is already filled, that no money is appropriated, and that the offer-with-strings repels the non-aligned states it targets.

Source List (grouped by theme)

China’s Belt and Road Initiative (scale and trajectory)

Council on Foreign Relations — China’s Massive Belt and Road Initiative (150+ countries, $1T+)

Green Finance & Development Center — BRI Investment Report 2025 (record 2025 engagement)

The “debt-trap” premise (contested)

Existing U.S. and allied counter-BRI machinery

DFC — Secures Expanded Authorities with FY26 NDAA ($205B cap, reauthorized through 2031, Dec 2025)

Partnership for Global Infrastructure and Investment — $600B G7 goal by 2027, counter-BRI

OECD — Blue Dot Network begins global certification framework for quality infrastructure

Part II — Congressional Debate Bill Analysis

What the bill does

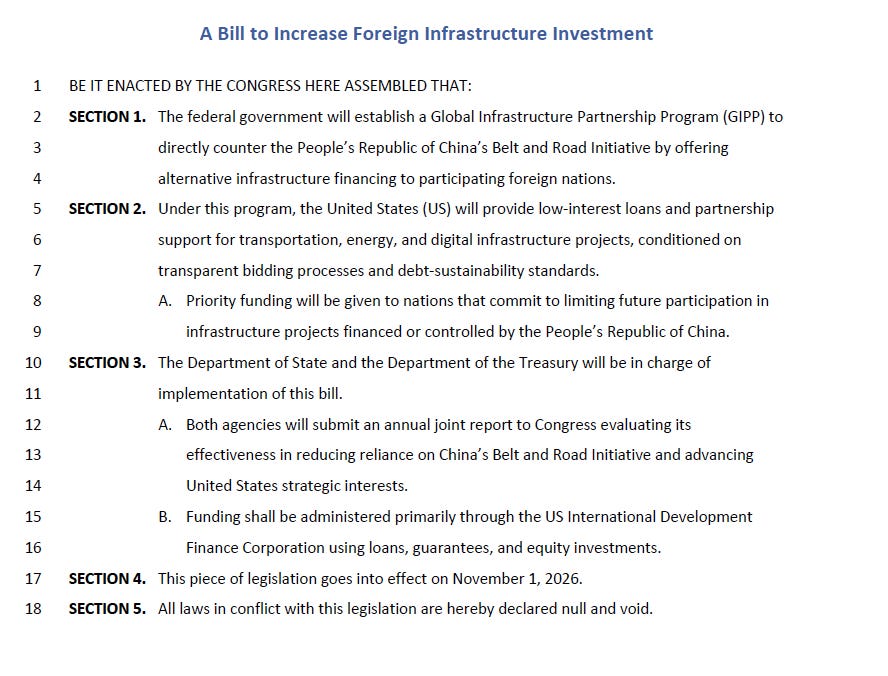

The bill creates a Global Infrastructure Partnership Program (GIPP) to counter China’s Belt and Road Initiative by offering participating foreign nations low-interest loans and partnership support for transportation, energy, and digital infrastructure, conditioned on transparent bidding and debt-sustainability standards. Section 2(A) gives priority to nations that commit to limiting future participation in Chinese-financed projects. State and Treasury implement it, funding is administered “primarily through” the DFC using loans, guarantees, and equity, and the two departments file an annual joint report to Congress. It takes effect November 1, 2026, and voids conflicting laws. The factual baseline both sides start from: the program’s named vehicle, the DFC, was reauthorized and expanded just months earlier, and the U.S. already runs two counter-BRI infrastructure efforts — so the bill builds on a field that is already occupied.

The strongest case for the bill

The advocates’ best ground is that the stakes are real, the demand is real, and the tool already works — so lead with the China threat, the fact the chamber accepts before any mechanism debate.

The first argument is the strategic stakes. BRI’s reach across 150-plus countries and $1 trillion-plus in financing gives Beijing leverage that becomes diplomatic and military influence, so a credible U.S. alternative is a national-security investment.

The second argument is demand. Many developing nations want infrastructure and would prefer transparent, debt-sustainable terms, so a program built on open bidding and sustainability standards meets a need that genuinely exists.

The third argument is feasibility. Routing money through the recently reauthorized DFC, with its loan, guarantee, and equity tools, means the program runs on proven, bipartisan machinery rather than a new agency built from nothing.

The fourth argument is differentiation. Competing on transparency and debt sustainability plays to American strength where BRI is weakest, letting the U.S. win on quality and governance instead of trying to match China dollar for dollar.

The fifth argument is leverage of private capital. Using loans, guarantees, and equity to mobilize private investment — the PGII model — stretches a modest federal commitment into a far larger financing footprint.

The sixth argument is accountability. The required annual State–Treasury report gives Congress a way to measure whether the program is actually reducing BRI reliance, a discipline most foreign-aid programs lack.

The strongest case against the bill

The opponents’ best ground is not “don’t compete with China” — lead with redundancy and the appropriation gap, then the loyalty-condition backfire.

The first and sharpest argument is the currency check: the bill recreates machinery that already exists. Its own vehicle, the DFC, was reauthorized to a $205 billion cap in December 2025, and the U.S. already runs PGII and the Blue Dot Network for this exact purpose. Most of the chamber won’t know the DFC was just expanded, so this point breaks.

The second argument is the procedural catch: the bill authorizes without appropriating. It promises “low-interest loans” with no dollar figure and no appropriation, routing through the DFC’s existing authorities and adding no new money — a named program with no funded commitment behind it.

The third argument is the mechanism mismatch. The DFC invests for returns and mobilizes private capital; it is not a concessional lender that issues below-market “low-interest loans,” so the bill asks the wrong agency to operate outside its statutory model.

The fourth argument is that the loyalty condition backfires. Section 2(A)’s priority for nations that limit Chinese participation turns a development offer into a loyalty test, and most BRI partners are non-aligned states that refuse binary choices — so the condition repels the very countries the program targets.

The fifth argument is that scale-matching is a losing frame. Even the expanded $205 billion DFC cap is dwarfed by BRI’s $1 trillion-plus and record 2025 activity, and this bill adds nothing to it — so a financing race accepts a contest the U.S. structurally can’t win.

The sixth argument is the contested premise. The bill is framed around countering debt traps, but Chatham House found the flagship Hambantota debt-trap story is largely a myth, so the animating rationale rests partly on a narrative the evidence doesn’t support.

The seventh argument is the muddled command structure. Section 3 makes both State and Treasury “in charge” while funding runs through the DFC — three institutions, no named lead, a coordination problem before the first project is financed.

Cross-examination questions

Questions for advocates to ask opponents.

“Do you dispute that BRI now reaches more than 150 countries with over a trillion dollars in financing — yes or no?”

“If transparent, debt-sustainable financing is a real alternative to BRI, why is creating a dedicated program to offer it a bad thing?”

“You say the DFC already exists — but the DFC’s mandate is returns, not strategic infrastructure diplomacy, so isn’t a purpose-built program exactly what’s missing?”

“Is your position that the United States should simply cede the infrastructure-financing contest to China?”

“The bill conditions support on transparency and debt sustainability — what’s your objection to financing that’s more responsible than BRI’s?”

“An annual report to Congress is built in — doesn’t that give us the accountability you say foreign aid usually lacks?”

Questions for opponents to ask advocates.

“The DFC — your bill’s own funding vehicle — was reauthorized to a $205 billion cap in December 2025. What does this program add that the DFC can’t already do?”

“Point me to the appropriation. How many dollars does this bill actually authorize, and where in the text is the money?”

“The DFC invests for returns; it isn’t a concessional lender. Which agency actually issues the ‘low-interest loans’ the bill promises?”

“We already run PGII and the Blue Dot Network as counter-BRI programs. Why isn’t this just a third name for the same thing?”

“Section 2(A) rewards nations that limit ties to China. If a country wants U.S. and Chinese projects both, does your program turn them away — yes or no?”

“Most BRI partners are non-aligned states. What’s your evidence the loyalty condition wins them over rather than pushing them toward Beijing?”

“BRI is over a trillion dollars and grew in 2025. If you can’t match that, why frame this as a financing race you’ve already lost?”

“Who is actually in charge — State, Treasury, or the DFC? The bill names all three.”

Drafting and definitional traps

The bill’s text rewards close reading and punishes the drafter.

“Low-interest loans” in Section 2 collides with Section 3(B), which routes funding through the DFC’s loans, guarantees, and equity — an institution built to invest for returns, not to issue concessional below-market loans. The operative financing term doesn’t match the operative agency.

There is no dollar amount and no appropriation anywhere in the text. The bill creates a program and names a vehicle but never funds either, so “will provide low-interest loans” is an authorization with nothing behind it.

Section 2(A)’s condition — priority for nations that “commit to limiting future participation in” Chinese-financed projects — is undefined at every edge. How much limiting counts? Is it enforceable? What happens to a nation that takes a U.S. loan and a Chinese one the next year? The text gives no answer.

The command structure names three masters. Section 3 puts State and Treasury jointly “in charge” and Section 3(B) adds the DFC as administrator, with no lead agency and no tie-breaker.

“Participating foreign nations” is never defined — no eligibility criteria, income thresholds, or governance requirements — so the universe of recipients is left entirely open.

The effective date of November 1, 2026, comes with no ramp or transition rule, and Section 5’s “all laws in conflict are hereby declared null and void” is decorative boilerplate that resolves nothing.

Logical flaws

The deepest problem is a redundancy non-sequitur. The bill’s premise is that the U.S. needs a vehicle to counter BRI; its conclusion is that Congress should build a new one — but the DFC was just reauthorized and expanded and PGII and Blue Dot already exist, so the premise (a gap) doesn’t support the conclusion (a new program) because the gap is already filled.

The conditionality contradicts the value proposition. The bill’s selling point is that U.S. financing is a better, more transparent offer — but if the offer is genuinely better, it should win on its merits, not require a pledge of exclusivity. Demanding that nations limit Chinese ties reframes the program as coercion rather than competition, undercutting its own premise that the U.S. wins on quality.

The scale framing is self-defeating. By positioning itself as a dollar-for-dollar answer to BRI while appropriating no money and adding nothing to the $205 billion DFC cap, the bill accepts China’s spending contest as the measure of success — a contest it structurally cannot win, so it defines itself by a standard it can’t meet.

The animating rationale rests on a contested factual premise. The bill leans on the “debt-trap” framing of BRI, but the flagship case for that framing has been substantially debunked, so even granting the strategic goal, the specific harm the bill invokes is weaker than it assumes.

Verdict / how to play it

The chamber will saturate the advocate side. “Stand up to China” is the easiest applause in Student Congress, and most competitors will run the BRI-threat statistics and the transparency framing without ever checking what the U.S. already does. Expect four or five advocacy speeches that never mention the DFC, PGII, or Blue Dot.

The rare and more valuable speech is the informed opposition: the one student who knows the DFC was reauthorized to $205 billion in December 2025 and that PGII and Blue Dot already exist, and who stands up to say the bill recreates programs already in the field, funds none of them, and bolts on a condition that drives partners away. That speech breaks because nobody else will have done the reading.

If you are advocating, do not pretend the field is empty — concede the DFC exists and argue the bill gives it a focused strategic mandate and a transparency-first identity that the returns-driven DFC lacks. Lead with the China stakes and the demand abroad, frame conditionality as leverage rather than coercion, and treat the bill as direction-setting, not a blank check.

If you are opposing, the highest-leverage move is the currency check run as one stroke: the DFC — the bill’s own vehicle — was just reauthorized to $205 billion, the U.S. already runs PGII and Blue Dot, and this bill adds no money to any of it, so it renames capability rather than adding it. Stack the loyalty-condition backfire behind it: a program premised on offering a better deal shouldn’t need to demand exclusivity, and demanding it repels the non-aligned states it targets. Hold the debt-trap-myth point for when an advocate leans hard on the framing.

Do not let the round collapse into “are you tough on China,” which the advocates win; force it onto “does this bill add anything the United States isn’t already doing, and is the loyalty condition smart or self-defeating,” which the opponents win. One cross-apply: this is a great-power-competition bill, so it pairs with any other China, foreign-aid, or strategic-financing measure in the docket under the same question of whether a new program adds capability or just a new name.