Why this fight is everywhere right now

Three years into the AI boom, data centers have gone from invisible infrastructure to the most contested land use in the country. The trigger is scale: building and equipping these facilities accounted for roughly 92% of U.S. GDP growth in the first half of 2025 by one Harvard economist’s estimate, even though the sector is about 4% of GDP — meaning that absent the buildout, measured growth would have been near zero. That same scale is what alarms the towns, utilities, and state legislatures now fighting over permits, water disclosure, and who pays for new power lines. The debate has produced real policy: California’s governor vetoed a water-disclosure bill in October 2025, Oregon is weighing legislation to make data centers pay their share of grid costs, and “moratorium” has entered the local-government vocabulary.

The contested question this brief works through is narrow and answerable: are the electricity and water demands of data centers a serious enough problem to justify slowing, restricting, or conditioning their development — or are those concerns overstated relative to the benefits and the industry’s ability to manage them? Both sides have real evidence. The honest difficulty is that the strongest version of each is partly true at different scales.

What data centers are and why we need them

A data center is a building full of servers, storage, and networking gear that processes and stores digital information. Roughly half or more of a data center’s power goes to the IT equipment itself, with much of the rest spent on cooling it. They are the physical substrate of everything from cloud storage and streaming to financial transactions, and — the reason demand suddenly spiked — the training and operation of AI models.

The case that the U.S. needs more of them rests on three points. First, the economic weight is now hard to overstate: the World Economic Forum estimates 80% of the rise in U.S. final private domestic demand in the first half of 2025 came from data centers and related high-tech spending, and hyperscalers (Microsoft, Amazon, Google, Meta) are on track for roughly $364 billion in capital investment in 2025, up from about $245 billion the year before. Second, the jobs and fiscal case: one industry-commissioned study estimated a $100 billion data-center buildout would create about 500,000 direct and indirect jobs and add $140 billion to GDP over five years. Third, the strategic frame: data-center capacity is the bottleneck on AI capability, and AI capability is increasingly treated as a competitiveness and national-security input, which is why states compete with tax incentives to land projects. A fair version of the case also notes the catch — the same Harvard economist cautioned that absent the AI boom the country would likely have lower interest rates and electricity prices, so some of the “growth” is a reallocation, and the assets depreciate fast.

The two pressure points: electricity and water

The resource numbers are the heart of the fight, so here is the verified baseline both sides argue from.

On electricity, the Congressionally-mandated 2024 LBNL/DOE report found U.S. data centers consumed about 4.4% of national electricity in 2023 (176 TWh, up from 58 TWh in 2014), and projected 6.7% to 12% by 2028 (325–580 TWh). The growth rate is the alarming part: a compound annual rate of about 7% from 2014–2018, jumping to 18% from 2018–2023, and forecast at 13–27% through 2028 — the inflection driven by AI servers. Globally, the IEA projects data-center electricity more than doubling from 415 TWh in 2024 to roughly 945 TWh by 2030.

On water, U.S. data centers directly consumed about 17 billion gallons in 2023, with hyperscale and colocation facilities using 84% of it, and hyperscale alone is projected to use 16–33 billion gallons a year by 2028. But the larger figure is indirect: water evaporated at the power plants supplying data-center electricity came to roughly 211 billion gallons in 2023, nearly ten times the on-site total. Both numbers exclude water used in chip manufacturing. The on-site figure carries a transparency caveat the LBNL authors themselves flag: the estimates rest on limited disclosure, and as of a 2016 survey fewer than a third of operators even tracked their water use.

The case that the concerns are serious

The strongest version of the worry is not “computers use power” — it’s that the rate and concentration of demand are outrunning the systems meant to absorb them, and that the costs land on people who get none of the benefit.

The growth rate broke the efficiency trend that used to save us

For roughly a decade, efficiency gains canceled out rising demand — data-center electricity stayed near 60 TWh from 2014 to 2018 even as workloads grew. AI broke that truce. LBNL documents demand more than doubling between 2017 and 2023 as AI servers scaled, with the growth curve steepening, not flattening. The concern-side point is that the reassuring “we always get more efficient” history no longer predicts the future, because chip power density is rising faster than efficiency can offset.

Ratepayers are subsidizing the buildout

This is the most concrete and verified harm. In the PJM grid region (Illinois to North Carolina), data centers were tied to an estimated $9.3 billion increase in the 2025–26 “capacity market”, translating to projected residential bill increases of about $18 a month in western Maryland and $16 in Ohio. A Carnegie Mellon analysis projects data centers and crypto could raise the average U.S. electricity bill about 8% by 2030, and over 25% in the highest-demand markets like northern Virginia. Against a backdrop of over $60 billion in U.S. rate increases in 2025, the equity problem is plain: utilities upgrade the grid for a handful of large customers, and absent ratepayer protections, households shoulder the cost.

Local water stress is the real harm, and national averages hide it

A national figure of “0.5% of industrial water” is cold comfort to a county where a single campus is the largest new draw. Texas data centers are projected to jump from 49 billion gallons in 2025 to as much as 399 billion by 2030 — the latter equivalent to drawing down Lake Mead by more than 16 feet in a year. Google reported 31% of its 2023 freshwater withdrawals came from medium- or high-scarcity watersheds, and northern Virginia’s data centers used close to 2 billion gallons in 2023, up 63% in four years. Evaporative cooling means much of that water doesn’t return as treatable wastewater — it’s gone. Siting water-hungry facilities in already-stressed basins recreates the exact vulnerability the “it’s a small share” framing waves away.

Opacity prevents accountability

The industry’s reluctance to disclose site-level water and power use — and the political muscle behind it, as when California’s disclosure bill was vetoed after industry opposition — means communities are asked to approve projects they can’t measure. The concern-side argument is that you cannot manage or trust what you cannot see, and that the burden of proof should sit with the operator, not the town.

The indirect footprint is the one nobody counts

Because the ~211 billion gallons of indirect water consumption happens at distant power plants, it never shows up in a data center’s reported “on-site” number. The same is true for the emissions of the natural gas that supplied over 40% of U.S. data-center electricity as of 2024. The concern-side point: the reassuring direct-use statistics systematically undercount the true resource footprint by an order of magnitude.

The case that the concerns are overstated

The strongest version of the rebuttal is not “there’s no impact” — it’s that the impact is small in proportion, falling fast per unit of compute, and largely an engineering-and-pricing problem rather than a reason to halt construction.

In proportion, the water use is minor — and shrinking per facility

Direct data-center water is about 0.5% of total U.S. industrial water consumption. For scale: thermoelectric power plants alone consumed roughly 962 billion gallons in 2022, dwarfing the entire data-center direct total. Brookings notes that training an advanced AI model uses less water than is applied to a single square mile of farmland in a year. The widely-shared “a bottle of water per AI prompt” figure comes from one 2023 UC Riverside estimate, and other estimates put it closer to a few spoonfuls — the metric is contested, not settled.

New cooling designs are approaching zero water

The water-intensive image comes from older evaporative cooling. The newest facilities use closed-loop and direct-liquid systems that recycle water continuously. Microsoft reports its next-generation designs consume essentially zero water for cooling once filled, and that its fleet water-use-effectiveness improved 39% from 2021 and 80% since its first generation. By one industry illustration, a new 100 MW closed-loop facility uses roughly 8,000 gallons a day — less than a tenth of what a 300-home subdivision on the same footprint would use. Closed-loop retrofits can cut freshwater use by up to 70%.

Energy efficiency is near its theoretical floor

Power Usage Effectiveness — total facility energy divided by IT energy — has fallen toward 1.0, with advanced hyperscale facilities operating below 1.1 and optimized deployments under 1.05. That means almost all the power now goes to computing rather than overhead. The rebuttal: the “runaway overhead” fear is dated; the marginal facility is far more efficient than the average one the alarming statistics are built on.

Data centers can strengthen the grid, not just strain it

Because large operators fund the grid upgrades their loads require, those investments can improve reliability and capacity for everyone on the same system. Hyperscalers are also the largest corporate buyers of renewable energy in the world, and increasingly co-locate generation — Meta and Ørsted are pairing a 300 MW solar field and battery array with a new Arizona campus. Where contracts require new clean generation that exceeds a site’s own use, the net effect on the grid can be positive.

The ratepayer problem is a rate-design problem, not a reason to stop building

The cost-shift is real, but the fix is targeted rather than prohibitionist: special large-load tariffs, “bring-your-own-generation” requirements, and cost-allocation rules that make data centers pay for the infrastructure they trigger. Oregon’s pending bill and similar efforts elsewhere aim at exactly this. The rebuttal frames a moratorium as overkill — it forfeits the economic and competitiveness gains to solve a problem that pricing already knows how to solve.

The bigger stake: would this slow AI itself?

The water-and-electricity fight is usually argued as a local environmental and ratepayer question. But the “overstated” case points toward a larger cost dimension the regulation debate often misses: because compute is the binding input to AI capability, constraining data centers can constrain AI progress itself — and AI progress is increasingly where large scientific, medical, and economic gains are coming from. This is the strongest version of the “go slow on regulation” argument, and the part of the debate where the “AI is good” claims do their work.

Compute is the binding input — cap the data center, cap the AI

Model capability tracks the compute and power available to train and run it; the constraint is increasingly physical rather than algorithmic. As one widely-shared framing puts it, the bottleneck in AI is not code — it is access to power and compute. A House Science Committee chairman opened a 2026 hearing on exactly this point, arguing that scaling AI is not just about smarter algorithms but about having the power to run them, with data centers consuming 183 TWh in 2024. And industry analysts describe compute capacity as a competitive moat where falling behind in compute equals falling behind in AI capability. The implication for this bill is direct: a per-facility cap on electricity or water is, functionally, a cap on the compute that trains and serves AI models. The regulation does not mention AI capability, but its binding constraint reaches it.

The “AI Good” payoff is already arriving, not hypothetical

The reason slowing AI carries a cost is that the benefits are concrete and present-tense, not promissory. The clearest proof point is AlphaFold: the 2024 Nobel Prize in Chemistry went to Google DeepMind’s Demis Hassabis and John Jumper — the first Nobel for an AI-enabled scientific breakthrough — for a system that predicted the structures of over 200 million proteins and has been used by more than two million researchers across 190 countries, accelerating drug discovery for cancer, Alzheimer’s, and neglected diseases like Chagas and leishmaniasis. Layer that on the economic engine already documented in this brief — the buildout driving roughly 92% of U.S. GDP growth in the first half of 2025 — and “forgone AI progress” stops being abstract. It cashes out as forgone medical, scientific, and economic gains, which is the real price tag on getting the regulation wrong.

The competitiveness cost — a unilateral brake in a race

The United States leads the AI frontier in compute scale and model performance, but Brookings describes the contest as multi-dimensional, and the U.S. lead runs through an energy bottleneck. By one account, data centers in China can be built in months rather than years and pay less than half the U.S. rate for electricity, while eight of thirteen U.S. regional grids sit at or below critical spare capacity. The argument is that unilateral U.S. resource caps risk either ceding ground in a race the country is trying to win or pushing capital toward friendlier jurisdictions. It is reinforced by the direction of federal policy itself: the 2025 AI Action Plan moves to streamline permitting and open federal land for data center development, so a bill imposing facility-level consumption caps and revenue-scaled penalties cuts directly against the national strategy of accelerating the buildout.

Regulatory drag is the mechanism, not an outright ban

No single rule bans AI. The slowing happens through friction: compliance cost, absolute per-facility caps, and outsized penalties — the AI Accountability Act’s 5%-of-revenue fine being the sharpest example — create the investment uncertainty that chills a fast-moving, capital-hungry buildout and diverts it elsewhere. In a sector where the marginal facility is the marginal model, drag on construction is drag on capability.

The honest limit of this argument

The chain from “regulate data centers” to “slow beneficial AI” has weak links, and a careful reader should hold the argument to its defensible version. Compute is not the only lever: efficiency can substitute for raw scale, and Chinese labs such as DeepSeek have produced competitive models from less compute, which undercuts any claim that constraining compute necessarily halts progress. The export-control experience points the same way — restrictions did not stop U.S. AI from scaling, with Nvidia’s valuation passing roughly $4 trillion. And a well-designed efficiency standard could lower the resource cost per unit of compute rather than cap capability, meaning regulation and AI progress are not strictly zero-sum. The defensible claim is therefore narrow: poorly designed resource caps — absolute per-facility limits, disproportionate penalties, the features this particular bill has — could slow beneficial AI, while smart efficiency standards need not. And the “AI is good” benefits, though real and in some cases Nobel-certified, are partly projected and unevenly distributed, which is a reason to weigh them seriously rather than treat them as a trump card.

How to weigh it

Strip away the rhetoric and the dispute reduces to a question of scale, distribution, and trajectory — and the two sides are largely arguing about different things, which is why both sound right.

The “overstated” case is strongest on national aggregates and per-unit trends: as a share of total water and as efficiency-per-computation, data centers are small and improving, and the worst statistics describe yesterday’s facilities. The “serious concern” case is strongest on local concentration and cost distribution: averages dissolve the problem of a single campus straining one watershed or one utility’s ratepayers, and the buildout’s growth rate has, for now, outrun the efficiency gains that used to keep total demand flat.

The crux: this is a dispute about whether the harms are diffuse-and-manageable or concentrated-and-externalized — and what raises the stakes of getting it wrong is that data-center capacity is also the binding input to AI progress, so a clumsy brake risks forgoing real scientific, medical, and economic gains, while a clumsy free pass leaves local water stress and ratepayer cost-shifts unaddressed. If you believe the impacts are spread thin across a national system that prices and engineers its way through them, restraint looks like self-sabotage. If you believe the impacts pile up on specific basins and specific ratepayers who never consented, then “it’s only 0.5% nationally” is precisely the move that lets the externality continue. The most defensible position the evidence supports is not a moratorium and not a free pass — it’s conditional approval: site away from stressed watersheds, mandate closed-loop cooling and disclosure, and require large-load tariffs so the people getting the power lines pay for them. That keeps the economic upside while closing the two externalities — local water stress and ratepayer cost-shift — that the “overstated” case never fully answers.

Applying the Framework: The Bill on the Floor

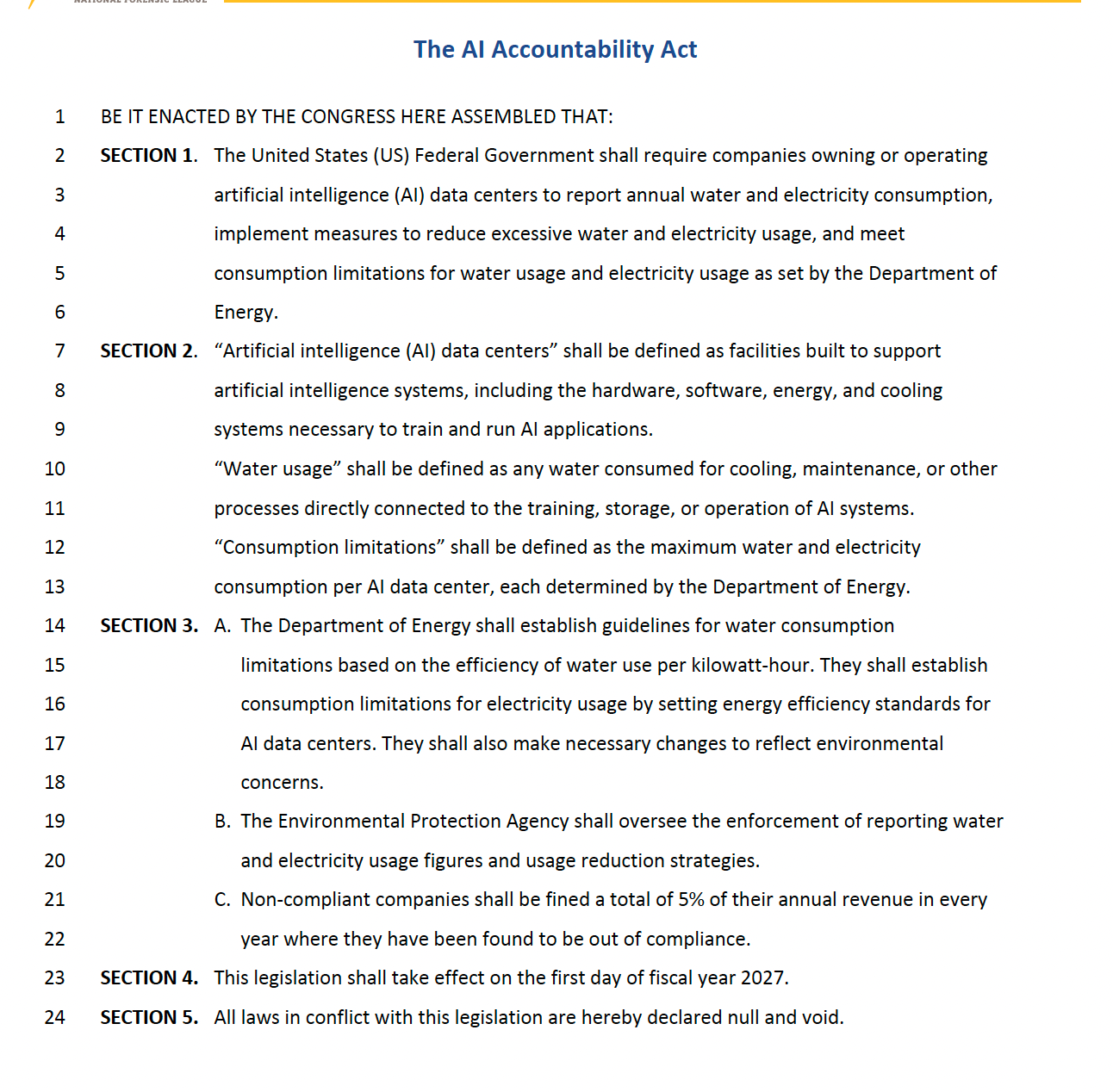

The evidence above isn’t abstract. Here is an actual piece of Congressional Debate legislation on exactly this question — The AI Accountability Act, which would require AI data centers to report water and electricity use, cut “excessive” usage, and meet Department of Energy consumption limits, with EPA enforcement and a 5%-of-revenue penalty, effective FY2027. It is analyzed for the chamber below: what it does, the strongest case on each side, the cross-examination, and where the drafting becomes a weapon. The evidence is the same as the brief above; the work here is turning it into a speech you can give on either side. Side terminology follows Congressional Debate convention: advocates argue the bill should pass, opponents argue it should not.

What the bill does

The bill orders the federal government to require companies that own or operate “AI data centers” to do three things: report annual water and electricity consumption, implement measures to reduce excessive use, and meet per-facility consumption limits set by the Department of Energy. DOE writes the standards — water limits keyed to efficiency per kilowatt-hour, electricity limits via energy-efficiency standards — while the EPA oversees enforcement of the reporting and reduction strategies. Non-compliant companies are fined 5% of total annual revenue for each year out of compliance. It takes effect the first day of fiscal year 2027 and declares conflicting laws null and void. It names no appropriation and no enforcer for the consumption limits themselves.

The strongest case for the bill

The advocates’ best ground is the transparency-and-externality frame — that the sector won’t disclose or self-limit voluntarily, and that the costs of inaction land on people who never consented. The first argument is the information gap: as of a 2016 survey fewer than a third of operators even tracked their water use, and California’s modest disclosure bill was vetoed in 2025 after industry opposition — so mandatory federal reporting fixes a market failure that towns and states demonstrably can’t. The second argument is the ratepayer externality, which is concrete and verified: data centers were tied to a $9.3 billion price increase in the PJM capacity market and projected residential increases of roughly $18 a month in parts of the region, so a federal floor stops a race to the most permissive state. The third argument is feasibility: efficiency standards have a track record at DOE, and leaders like Microsoft already run near-zero-water cooling, so the bill codifies a best practice the frontier of the industry has shown is achievable, not a fantasy. The fourth argument is that accountability without teeth is theater — a penalty smaller than the cost of compliance is just a pollution license, so a revenue-scaled fine is what makes even a trillion-dollar company treat the limit as real. If you’re advocating, lead with the transparency gap and the ratepayer harm; both are verified and neither is easily rebutted, and they let you frame opponents as defending secrecy and cost-shifting.

The strongest case against the bill

The opponents’ best ground is not “regulation bad” — it’s that the bill is so loosely drafted that it can’t hit what it aims at, punishes out of all proportion, and steps on authority it doesn’t have. The first argument is the unworkable definition: an “AI data center” is one “built to support AI systems,” but modern hyperscale facilities run cloud storage, streaming, and AI on the same machines, so the bill regulates a category that doesn’t cleanly exist and invites evasion by relabeling — a company need only characterize a facility as general-purpose. The second argument is that the water definition misses the target: it covers only water “directly connected” to AI, yet the indirect water consumed at power plants is roughly ten times the on-site amount (about 211 billion gallons versus 17 billion in 2023, per Berkeley Lab 2024), so the bill ignores the larger part of the footprint it claims to police. The third argument is the penalty: 5% of total annual revenue — for a company with several hundred billion in revenue, that is tens of billions for a single facility-year — bears no relationship to the environmental harm and is the kind of grossly disproportionate fine the Supreme Court warned against in United States v. Bajakajian (1998), where it held a penalty must be proportional to the gravity of the offense. The fourth argument is the enforcement gap: the EPA is assigned to enforce reporting, but no agency is assigned to enforce the consumption limits themselves, and DOE — an energy-efficiency body — is handed authority over water standards that sit closer to EPA and the states. The fifth argument is federalism: water allocation is governed by state law, so a federal cap on how much water a facility in Texas or Arizona may use intrudes on authority the states have always held. The sixth is the procedural one: the bill imposes new rulemaking and enforcement duties on two agencies and appropriates nothing to fund them. If you’re opposing, open with the definition and the penalty — both are facial, both are in the text, and the penalty in particular will strike most of the chamber as obviously excessive once you put a dollar figure on it.

Cross-examination questions

Questions for opponents to ask advocates:

“Section 2 defines an ‘AI data center’ as one ‘built to support AI systems.’ A hyperscale facility runs cloud, streaming, and AI on the same servers. Who decides whether it counts, and what stops a company from saying it wasn’t built for AI?”

“Your water definition covers water ‘directly connected’ to AI. Berkeley Lab found indirect water at power plants is about ten times the on-site amount. Why does your bill ignore the larger share of the footprint?”

“Section 3C fines 5% of annual revenue. For a company with $600 billion in revenue, that’s $30 billion for one facility-year. Is that proportioned to the environmental harm, or to the company’s size?”

“Section 2 sets a ‘maximum consumption per data center,’ but Section 3A keys the standard to efficiency ‘per kilowatt-hour.’ Which governs — an absolute cap or an efficiency rate? They are not the same thing.”

“Section 3B has EPA enforce reporting. Which agency enforces the consumption limits themselves?”

“Where does the bill appropriate money for DOE to write these standards or for EPA to enforce them?”

“Water rights are set by the states. What is your federal authority to cap how much water a given facility may use?”

Questions for advocates to ask opponents:

“Do you dispute that fewer than a third of operators even tracked their water use? If the market won’t disclose voluntarily, how do communities get the information?”

“California’s disclosure bill was vetoed after industry lobbying. Without a federal floor, what stops companies from shopping for the most permissive state?”

“Microsoft already runs near-zero-water cooling. If best practice is this achievable, why shouldn’t a federal standard require it?”

“A fine smaller than the cost of compliance is a license to pollute. What penalty actually changes a trillion-dollar company’s behavior?”

“PJM households saw a $9.3 billion data-center-driven price increase passed to them. Is doing nothing your answer to that?”

“DOE already sets energy-efficiency standards that work. Why can’t it set them for data centers?”

Drafting and definitional traps

The text rewards close reading in four places. First, the “AI data center” definition in Section 2 has no workable boundary — it keys on a facility being “built to support AI systems,” but workloads are mixed and fungible, so the regulated category blurs into every large data center and invites relabeling. Second, “water usage” is defined as water “directly connected” to AI, which by the verified numbers excludes roughly ninety percent of the real water footprint (the indirect use at power plants). Third, the bill contradicts itself on the metric: Section 2 sets a “maximum consumption per AI data center” (an absolute cap), while Section 3A sets standards based on “efficiency of water use per kilowatt-hour” (an intensity rate) — these pull in opposite directions, and a hyper-efficient mega-facility could be best-in-class per kWh while blowing through an absolute cap. Fourth, “excessive” usage in Section 1 is never defined, and “make necessary changes to reflect environmental concerns” in Section 3A hands DOE open-ended discretion with no intelligible standard for how much is too much.

Logical flaws

The reasoning problems run deeper than the wording. The central one is a targeting failure: the bill’s title promises accountability for water and electricity, but its own water definition reaches only the smaller, direct portion and ignores the indirect portion that is an order of magnitude larger — so the mechanism cannot reach the harm it names. The second is the arbitrary carve-out: regulating “AI data centers” but not physically identical non-AI data centers rests on a distinction that doesn’t survive contact with how facilities actually run mixed workloads, so the bill can be evaded by characterization, defeating its purpose. The third is the penalty’s non-sequitur: a flat 5% of total corporate revenue tracks company size rather than violation severity, so two identical violations produce wildly different fines and a minor overage is punished as harshly as a gross one — the opposite of the proportionality Bajakajian (1998) requires. The fourth is the enforcement gap that empties the bill of force: EPA is told to enforce reporting, but the consumption limits — the heart of the bill — have no named enforcer, so the binding part of the statute is left unattended. The fifth is an internal-competence mismatch: DOE is assigned water-efficiency standards despite being an energy body, while EPA, the natural water regulator, is limited to enforcing paperwork — the agencies are pointed at the wrong halves of the problem.

Verdict / how to play it

The chamber will split on predictable lines: this reads as “hold Big Tech accountable” versus “government overreach kills American AI,” and at a moment when data centers are politically charged, both sides have ready applause. Advocates will flood the accountability framing; opponents will flood the innovation-and-overreach framing. The break, as usual, is the technically literate speech. For opponents, the highest-leverage move is not ideological — it is the definitional-and-enforcement autopsy: the AI-versus-non-AI line is unworkable, the water definition misses most of the footprint, and nobody enforces the caps. The 5%-of-revenue penalty is your single cleanest point, because once you attach a real dollar figure to it the disproportion is self-evident and Bajakajian gives it a legal name. For advocates, do not die defending the text — concede the drafting and pivot to the principle plus friendly amendments: redefine the target by facility size rather than “AI,” extend the water definition to indirect use, scale the penalty to the violation, and name a single enforcer. Then stand on your two strongest and least-rebuttable facts — the transparency gap the market won’t close and the ratepayer cost-shift already hitting households. The single best point on each side is symmetric: for opponents, the penalty and the enforcement gap; for advocates, the verified externality that does real harm right now. Cross-apply the whole brief above — the advocate runs the “concerns are serious” section, the opponent runs the “overstated” section, and the point that the harm is local while this bill is national and blunt.

Source List (grouped by theme)

Electricity demand (baseline and projections)

DOE — 2024 Report on U.S. Data Center Energy Use (4.4% in 2023, 6.7–12% by 2028)

Mobius — breakdown of the LBNL growth-rate forecasts (CAGR 7%→18%→13–27%)

CRS — Data Centers and Their Energy Consumption FAQ (R48646)

GlobeNewswire — IEA projection (415 TWh 2024 to ~945 TWh by 2030)

Water use

Pew Research — energy and water at U.S. data centers (17B gallons 2023; hyperscale 16–33B by 2028)

Bluefield Research — direct vs. indirect water; 0.5% of industrial use; 211B gallons indirect

EESI — data centers and water consumption (power-plant comparison; closed-loop savings)

Lincoln Institute — Texas projections, Google scarcity-watershed data, per-prompt dispute

Brookings — global energy/water in the AI regulatory landscape (farmland comparison)

Economic case

Ratepayer and policy

Efficiency, cooling, and the “overstated” case

DCD — sorting fact from fiction (PUE, closed-loop, grid benefits)

Microsoft — next-generation zero-water cooling and WUE figures

Bill analysis (legal anchor)

AI progress, compute, and competitiveness (”AI Good”)

Nature — 2024 Chemistry Nobel for AlphaFold (Hassabis, Jumper, Baker)

AI Magazine — AlphaFold: 200M+ proteins, 2M+ researchers across 190 countries

House Science Committee — compute and power as the AI bottleneck (2026)

Brookings — Competing AI strategies for the US and China (efficiency vs. scale)

ARI — strategic inputs in U.S.–China AI competition; the AI Action Plan